A critical analysis of the failure of the European Council in addressing the Covid-19 crisis, by Andrea Del Monaco, author and expert in EU funds.

According to Marx[1] (quoting Hegel), major events and figures appear twice: first as tragedy, then as farce. Just as Napoleon I’s Bonapartism appeared again in his nephew Napoleon III, Mussolini’s fascism is, in a new form, reoccurring in Giorgia Meloni and Matteo Salvini. If the EU is to respond to the economic emergency created by Covid-19 only with the solution offered by the last European Council, which provided no resources, Salvini and Meloni will get the vote of the newly unemployed and of bankrupt small businesspeople, similar to the deflationary policies of Chancellor Brüning in 1930-32 resulted in Hitler’s accession to power, the EU’s ordoliberalism, absent a strong Italian left, can allow Salvini and Meloni to win. Why? Because Angela Merkel, Mark Rutte, and Sebastian Kurz won the last European Council. Their ordoliberalism informs the meagre 23 April press release by President Charles Michel, which turns around three points:

a) approval of the 540 billion euro package proposed in the Eurogroup on 9 April, which goes into effect 1 June;

b) the generic reference to the creation of a recovery fund;

c) the absence of Eurobonds.

The 540 billion of the package will be divided as follows: 200 billion from the European Investment Bank (EIB), 100 billion from the SURE initiative (Support to Mitigate Unemployment Risks in an Emergency), and 240 billion from the European Stability Mechanism. In reality, there are no 540 million and no fresh money as this is all offset by the financial obligations countries like Italy will incur if they accept help. Let’s look more closely at the Eurogroup’s 9 April report cited by Charles Michel on 23 April.

1. EBI: formally 200 billion in loans to SMEs, in reality only 12 billion fresh funds

The economic ministers state:

‘We welcome the initiative of the EIB Group to create a pan-European guarantee fund of EUR 25 billion, which could support EUR 200 billion of financing for companies with a focus on SMEs, throughout the EU, including through national promotional banks.’[2]

Concretely, there are only 25 billion in guarantees. And these guarantees are supposed to induce all European banks to serenely loan 200 billion to the small and medium-sized enterprises hurt by the crisis. Invaluable in letting us understand this is the Note of the Italian Senate no. 44/2 entitled The Covid Epidemic and the European Union, where four EIB interventions for supporting small and medium-sized enterprises are highlighted, specifically:

1) programmes of collateral to the banks, based on those already in existence and capable of being rapidly implemented, which would allow a mobilisation of up to 20 billion euros of financing for enterprises, but it is not clear how much fresh money is being allocated.

2) An acceleration and change of destination for lines of credit to banks that can convey these specifically to enterprises hurt by the crisis. The financing by the EIB will total 5 billion euros and can permit the mobilisation of 10 billion for enterprises – here the fresh money is 5 billion.

3) Two billion euros in programmes for buying asset-backed securities (ABS), via resources of the European Investment Fund for strategic investments, to allow banks to guarantee the risk on loans for the SMEs and thus to mobilise additional support of 10 billion euros – here the fresh money amounts to only 2 billion.

4) Measures to pay for healthcare infrastructure, systems, and equipment tapping 5 billion of EIB reserves for healthcare projects – here there are in fact 5 billion in fresh money.

Thus, to recapitulate, the fresh money totals € 12 billion (5+2+5).

2. SURE: Formally, 100 billion for unemployment benefits, in reality only 25 billion in guarantees if the EU states pay it

On 9 April the Eurogroup welcomed the Commission’s 2 April proposal ‘COM(2020) 139 final’ to establish a ‘temporary instrument supporting Member States to protect employment in the specific emergency circumstances of the COVID-19 crisis’.[3] Unemployment benefits in Italy would be paid through ‘loans granted on favourable terms from the EU to Member States, of up to EUR 100 billion in total’.[4] The European Commission would be authorised to borrow up to a maximum of 100 billion euros on behalf of the Union by means of issuing securities in the capital markets or directly from financial institutions. The devil is in the details. The Commission’s 2 April proposal – COM(2929) 139 (Article 12) – is clear: ‘The financial assistance referred to in Article 3 shall only become available after all Member States have contributed to the Instrument with contributions referred to in Article 11(1) for an amount representing at least 25 per cent of the amount referred to in Article 5’ – 25 per cent of € 100,000,000,000 amounting to € 25 billion, according to the share of Member States in the Gross National Income of the Union. But note: SURE will be activated only after the EU Member States have paid in their share of the 25 billion as a guarantee for a loan of 100 billion!

3. No to debt with the ESM that could force Italy to pay up to 111 billion and deliver itself into the hands of the Troika

With the European Stability Mechanism, the finance ministers are creating support based on the precautionary ECCL (Enhanced Conditions Credit Line):

‘The only requirement to access the credit line will be that euro area Member States requesting support would commit to use this credit line to support domestic financing of direct and indirect healthcare, cure and prevention related costs due to the COVID 19 crisis. The provisions of the ESM Treaty will be followed. Access granted will be 2% of the respective Member’s GDP as of end-2019, as a benchmark.'[5]

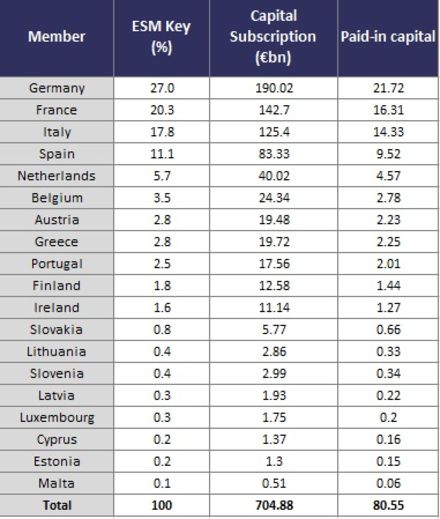

Italy will be able to get a loan of up to 36 billion – only for healthcare assistance, not for the economic emergency. What are the ESM provisions that need to be followed according to the treaty in force? As shown by the table below, the total capital subscription amounts to 704.88 billion euros, the paid-in capital amounts to 80.55 billion. In terms of the total capital subscription, Italy is the third contributor with 125.4 billion euros (17.7%) after Germany (190 billion) and France (142 billion). In terms of capital paid in, Italy has paid 14.3 billion euros, Germany 21.7 billion, and France 16.3 billion.

Capital Contribution of ESM Member States

Source: ESM website; own modification

Note:

Member States ranked after Capital Subscription; Capital contribution keys as shown above effective from February 2019; Paid-in capital refers to the final amount once all of the five instalments have been paid; Due to the rounding, some differences may exist between subcomponents and the total sum;

This is the crux: According to Article 8 of the ESM, ‘The obligations of ESM Members to contribute to the authorised capital stock in accordance with this Treaty are not affected if any such ESM Member becomes eligible for, or is receiving, financial assistance from the ESM.’[6] According to Article 12, paragraph 1:

‘If indispensable to safeguard the financial stability of the euro area as a whole and of its Member States, the ESM may provide stability support to an ESM Member subject to strict conditionality, appropriate to the financial assistance instrument chosen. Such conditionality may range from a macro-economic adjustment programme to continuous respect of pre-established eligibility conditions’.

Thus the minimum condition for the ESM is a programme of macroeconomic structural adjustments, that is, a Memorandum dictating cuts similar to those imposed on Greece in 2015. Therefore:

1) At any given moment the ESM’s Board of Governors can ask Italy for the difference between the authorised capital, 125.4 billion, and the capital paid in, 14.3 billion, which is to say up to 111 billion (125.4 – 14.3 = 111.1).

2) We would have to ask the EMS for a loan to face the economic emergency.

3) At the same time we would have to contribute to the capital of the EMS that is lending us the money.

4) And, in any case, we would have to subscribe to a Greek-style Memorandum. The same fate can befall Spain, from which the Board of Governors could demand 73.8 billion, the difference between the capital paid in and the capital subscription (83.3 – 9.5).

Why Merkel rejects Eurobonds

Merkel does not want Eurobonds because they would put an end to the spread between Italy’s BTPs and the German Bund and because she trusts in the conditions imposed by the EMS. Merkel, Rutte, and Kurz are officially opposed to the Eurobond because they do not want to incur part of the current and future Italian debt. The actuality is different. Unfortunately, the Euro is not the Dollar. The Dollar is a currency – in its area interest rates are substantially homogenous. By contrast the euro is a system of fixed exchange rates: 19 states hold the euro, with 19 different rates of interest on debt and different spreads among the 19 state bonds of the 19 Member States. Today we have BTPs, Bunds (the name of Germany’s and Austria’s state bonds), and Bonos (Spanish state bonds) with different yields and interest rates. Some Bunds have negative yields, that is, those who buy them do not receive interest but pay interest in order to keep them. In this way Germany finances itself at zero or even negative interest. What does this mean? Italy (and Spain) pays interest to those who buy its debt. By contrast, with the same currency, Germany receives interest from those who buy its debt. But note: If the ECB were to issue Eurobonds for the coronavirus, that is, guaranteed European securities at low to nil interest rates, even Italy and Spain could finance their debt at almost no interest. It would be the beginning of the end of the BTP-Bund spread. Italian or Spanish businesses would have loans in the bank with interest rates equal to the low rates the German or Dutch companies pay. The same would happen with home mortgages. Germany, Austria, and Holland would lose the exclusive privilege of financing their own debt at zero interest. This is why they are opposed to Eurobonds. And they propose the EMS because the EU Council can always impose conditionalities by a qualified majority ex post. Italy will not be able to impose a veto. Indeed, according to Article 7, Comma 5 of the Regulation 472/2013 of the European Parliament and of the Council,

Footnotes

[1] Karl Marx, The Eighteenth Brumaire of Louis Bonaparte, in Karl Marx and Frederick Engels, Collected Works, vol. 11, New York: International, 1978, p. 103.

[2] Council of the EU, Report on the comprehensive economic policy response to the COVID-19 pandemic, <https://www.consilium.europa.eu/it/press/press-releases/2020/04/09/report-on-the-comprehensive-economic-policy-response-to-the-covid-19-pandemic/pdf>, paragraph 15.

[3] Council of the EU, Report on the comprehensive economic policy response to the COVID-19 pandemic, paragraph 17.

[4] Ibid.

[5] Ibid., paragraph 16.

[6] <https://www.esm.europa.eu/sites/default/files/20150203_-_esm_treaty_-_en.pdf>, Article 8, Paragraph 5.